Car Buying & Negative Equity | Everything You Need To Know

Negative Equity Can Be Scary, If You Don’t Fully Understand It. Here’s What It Really Means

Buying a car should be exciting. Whether you're upgrading to something newer, making room for a growing family, or finally getting behind the wheel of the model you've been eyeing for months, it's usually a positive experience.

But for many drivers, there's one financial detail that can turn a straightforward purchase into a much more complicated conversation: negative equity.

If you've ever been told you have negative equity in your current car, or you've wondered why a dealer says you still owe money even though you're trading your vehicle in, you're not alone. It's one of the most misunderstood parts of car buying and car finance.

The good news is that negative equity isn't unusual, and it doesn't automatically mean you're in financial trouble. It simply means you need to understand what's happening before signing on the dotted line.

Here's everything you need to know.

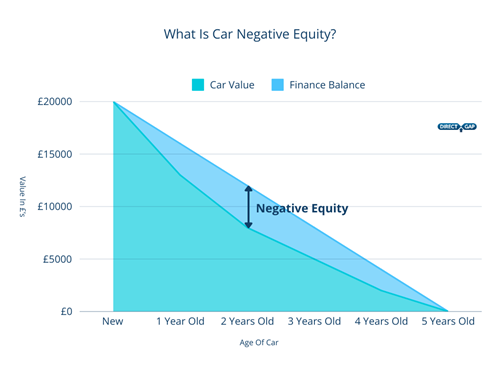

What Is Negative Equity?

Negative equity occurs when your car is worth less than the amount you still owe on it.

Imagine you have £12,000 left on your finance agreement, but your car's current market value is only £10,000. In that situation, you have £2,000 of negative equity.

In simple terms, if you sold the car today, the sale proceeds wouldn't fully clear the finance balance.

Negative equity is extremely common with financed vehicles because cars tend to lose value quickly, especially during the first few years of ownership. Research shows that many new cars lose between 15% and 35% of their value in the first year alone, with depreciation continuing steadily afterwards.

The gap between what the vehicle is worth and what you still owe is what creates negative equity.

Why Does Negative Equity Happen?

Most cases of negative equity come down to depreciation. Cars are depreciating assets (excluding rare cases). Unlike property, which may increase in value over time, most vehicles gradually become worth less as they age.

Several factors can accelerate that decline:

- High annual mileage

- Poor condition or accident damage

- Choosing a model with weaker resale values

- Long finance agreements

- Small deposits

- Changes in market demand

A five-year finance agreement may keep monthly payments lower, but it can also mean you repay the loan more slowly. If the car's value falls faster than the outstanding finance balance, negative equity can appear.

This is particularly common during the first half of a finance agreement when much of your monthly payment is covering interest rather than reducing the capital balance.

How Can You Tell If You Have Negative Equity?

The calculation itself is straightforward.

First, find out:

- Your finance settlement figure.

- Your car's current market value.

Then compare the two.

For example:

- Outstanding finance balance: £14,000

- Current vehicle value: £11,500

- Negative equity: £2,500

Many finance companies can provide a settlement figure online or over the phone. To estimate your car's value, it helps to obtain several valuations from reputable sources rather than relying on a single figure. Try tools like Auto Trader and We Buy Any Car for a quick, online valuation.

It's worth remembering that dealer trade-in values are often lower than private sale values, so the amount of negative equity can vary depending on how you sell the vehicle.

Read More: If you’re considering selling, read our guide; Should I Trade In Or Sell Privately, for an indepth look at the pros and cons of both.

Is Negative Equity A Problem?

Not always, but there are some select scenarios where it can cause major headaches and financial difficulty.

Many drivers have some degree of negative equity at various stages of ownership. The real issue arises when you want to change vehicles before the finance agreement ends.

If you're planning to keep the car until the finance is paid off, negative equity may simply reduce over time as your balance falls and the depreciation curve slows.

Problems usually arise when:

- You want to trade the vehicle in early

- You need to sell unexpectedly

- The car is written off and insurance doesn't cover the outstanding finance

- You're looking to refinance or change agreements

Understanding where you stand financially allows you to make informed decisions rather than being caught out by an unexpected shortfall.

Can You Trade In A Car With Negative Equity?

Yes.

In fact, dealers handle negative equity transactions every day. The most common solution is for the shortfall to be added to your next finance agreement. Often known as ‘rolling over’ negative equity.

Let's say:

- Your current car is worth £8,000

- Your settlement figure is £10,000

- Negative equity is £2,000

If you buy another vehicle, that £2,000 shortfall may be incorporated into the new finance package.

While this can make upgrading easier, it's important to understand the consequences.

You'll effectively be financing part of your old vehicle's debt alongside the cost of the new one.

That means:

- Higher monthly payments

- A larger total amount borrowed

- Potentially paying interest on the negative equity

For some drivers, it makes sense. For others, it can create a cycle where negative equity follows them from one vehicle to the next.

Read More: Trading a car in with a dealership is different to selling privately. We’ve covered this in more detail in Buying, Selling & Trading In A Car With Outstanding Finance.

The Hidden Risk Of ‘Rolling’ Negative Equity Forward

Rolling negative equity into a new agreement isn't automatically a bad decision.

Sometimes circumstances change. A larger family, a new job or reliability concerns may mean changing vehicles is the practical choice.

The risk comes when negative equity is repeatedly carried forward.

Imagine carrying a £2,000 shortfall into a new agreement. Then, a few years later, carrying another £2,000 shortfall into the next vehicle.

Over time, you can end up financing thousands of pounds from previous cars without realising how much extra debt has accumulated.

This is why understanding the numbers before agreeing to a new deal is so important.

A lower monthly payment can sometimes disguise a much larger overall borrowing figure.

Negative Equity And PCP Agreements

Negative equity often comes up in discussions around Personal Contract Purchase (PCP) agreements. At the end of a PCP agreement, your vehicle's value plays a significant role in determining your options.

If the car is worth more than the Guaranteed Minimum Future Value (GMFV), you may have positive equity available.

If the vehicle's value is lower than expected, equity may be limited or non-existent.

Many drivers use any positive equity as a deposit towards their next vehicle. When that equity isn't available, it can come as a surprise.

Market conditions can influence this considerably. During periods when used car prices are strong, equity positions often improve. When values soften, negative equity becomes more common.

A Note About GMFV

Whilst the GMFV is just that, a guarantee of your car’s future value, to ensure you’re never handing a car back that owes money (at the end of your PCP), many drivers don’t realise that there are some conditions where that can happen.

Damage or higher than forecasted mileage are both factors which could mean your car is worth less than the Guaranteed Future Value. Cosmetic protection products, such as Tyre & Alloy Wheel Insurance and Scratch & Dent Cover (also known as ‘SMART’ cover) can help minimise this risk, as they can ensure your car is returned as expected for it’s final inspection.

Read More: How To Prepare Your Car For PCP End-Of-Term Inspection.

Can You Avoid Negative Equity Altogether?

It's difficult to eliminate the risk completely, but you can reduce the chances significantly.

- Put Down A Larger Deposit: A larger deposit means borrowing less from the outset. Because the finance balance starts lower, it's easier for repayments to keep pace with depreciation.

- Choose Cars With Stronger Residual Values: Some vehicles hold their value better than others. Popular models with strong reliability reputations and healthy used-car demand often depreciate more slowly than niche or luxury alternatives.

- Avoid Changing Cars Too Frequently: The steepest depreciation usually happens during the first few years of ownership. Many vehicles lose 40% to 60% of their value within their first three years.Keeping a car for longer allows depreciation to level out and gives more time to reduce the finance balance.

- Consider Agreement Length Carefully: Longer agreements reduce monthly payments but can increase the likelihood of negative equity during the early and middle stages of ownership

There's often a balance between affordability today and flexibility later.

What Happens If Your Car Is Written Off While In Negative Equity?

If your car is declared a total loss following an accident or theft, your motor insurer will usually pay the vehicle's market value at the time of the claim. They don't generally settle the finance balance.

Here’s an example:

- You have outstanding finance on your car of £18,000

- When it’s written off, thanks to depreciation, the insurance payout values the car at £15,000 at the time.

That’s a remaining £3,000 shortfall which may still need to be paid.

As vehicles often depreciate faster than finance balances reduce during the early years of ownership, this situation is more common than many people realise.

It's one reason why motorists consider GAP insurance, which is designed to help bridge certain financial shortfalls following a total loss, depending on the policy purchased and individual circumstances.

Return To Invoice insurance in particular, is designed to cover the difference between your settlement figure and the invoice price of your vehicle, which covers finance.

Should You Pay Off Negative Equity Before Changing Cars?

If possible, paying off the shortfall separately can often be the most financially efficient approach.

Doing so may:

- Reduce overall borrowing

- Lower monthly payments

- Avoid paying additional interest on old debt

- Improve future finance options

Of course, not everyone has spare cash available to clear negative equity immediately.

In those cases, understanding the full cost of rolling it into a new agreement becomes especially important.

Ask for clear figures showing:

- The amount of negative equity being carried forward

- The total amount being financed

- The total repayable amount

- Any changes to monthly payments

The decision should be made entirely by you. We recommend doing your research thoroughly before making any long term financial decisions.

Common Myths About Negative Equity

"Negative equity means I'm trapped"

Not necessarily.

You may still be able to sell, trade in or refinance the vehicle. The key issue is understanding how any shortfall will be dealt with.

"Every financed car has negative equity"

Many do at some stage, but not all.

Strong deposits, shorter finance terms and good residual values can reduce the likelihood.

"It's only a problem with expensive cars"

Negative equity can affect vehicles at almost any price point.

It's determined by the relationship between value and outstanding finance, not simply by how much the vehicle costs. Our Top 10 Most Depreciating Cars list shows how diverse makes and models can be, whilst still being susceptible to losing value.

"Dealers make up negative equity figures"

The calculation itself is relatively simple. The difference between your settlement figure and your vehicle's market value determines the position. The important part is ensuring the valuation used is realistic.

Our Final Word

Negative equity is one of those phrases that sounds more alarming than it really is.

At its core, it simply means your vehicle is worth less than the finance balance attached to it.

For many drivers, that's a normal stage of car ownership. The challenge comes when changing vehicles, selling early or dealing with an unexpected write-off.

Understanding how negative equity works puts you in a much stronger position when buying your next car. It allows you to compare finance options properly, assess trade-in offers with confidence and avoid carrying unnecessary debt forward.

The numbers matter more than the terminology.

Before agreeing to any new finance agreement, take the time to understand exactly what your current vehicle is worth, how much you still owe and whether any negative equity is being included in the deal. A few minutes spent checking the figures can save a considerable amount of money over the life of the agreement.

As always, if you've enjoyed reading this, please share it with your friends & network.

Pin It!

Luke Sanderson

Luke is our resident copywriter, combining plenty of automotive experience, particularly in car sales with a commitment to well-researched, extensive writing. He draws on his own experiences, as well as quizzing the entire team at Direct Gap to ensure the blogs and articles you read are worthwhile, valuable and accurate. Got a question for Luke? Drop us a DM on social media and he'll be happy to help.